(See related pages)

Now that the various elements of financial statements have been identified, we discuss when they should be recognized (recorded) and how they should be measured. SFAC 5 addresses these issues. Recognitionprocess of admitting information into the basic financial statements. refers to the process of admitting information into the basic financial statements. Measurementprocess of associating numerical amounts to the elements. is the process of associating numerical amounts to the elements. For example, a revenue was previously defined as an inflow of assets from selling a good or providing a service. But, when should the revenue event be recorded, and at what amount? RECOGNITIONAccording to SFAC 5, an item should be recognized in the basic financial statements when it meets the following four criteria, subject to a cost effectiveness constraint and materiality threshold:

These obviously are very general guidelines. The concept statement does not address specific recognition issues.

MEASUREMENTThe question of measurement involves two choices: (1) the choice of a unit of measurement, and (2) the choice of an attribute to be measured. SFAC 5 essentially confirmed existing practice in both of these areas. The monetary unit or measurement scale used in financial statements is nominal units of money without any adjustment for changes in purchasing power. In addition, the board acknowledged that different attributes such as historical cost, net realizable value, and present value of future cash flows are presently used to measure different financial statement elements, and that they expect that practice to continue. For example, property, plant, and equipment are measured at historical cost; accounts receivable are measured at their net realizable value; and most long-term liabilities, such as bonds, are measured at the present value of future cash payments. Present value measurements have long been associated with accounting valuation. However, because of its increased prominence, present value is the focus of a recent FASB concept statement that provides a framework for using future cash flows as the basis for accounting measurement and also asserts that the objective in valuing an asset or liability using present value is to approximate the fair value of that asset or liability.38 We explore this objective in more depth in Chapter 6.

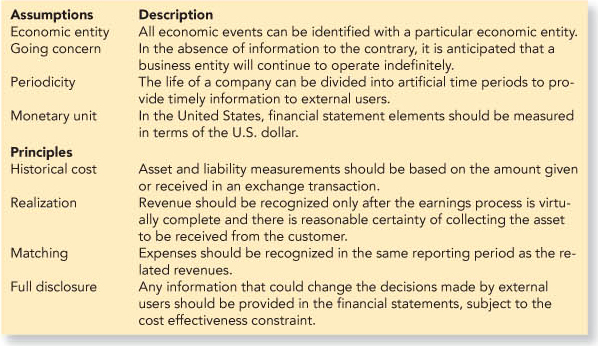

Answers to the recognition and measurement questions are imbedded in generally accepted accounting principles. SFAC 5 confirmed some of the more important of these principles used in present practice. GAAP consist of broad principles and specific standards. The accrual accounting model is an example of a broad principle. Before addressing additional key broad principles, we look at some important assumptions that underlie those fundamental principles. UNDERLYING ASSUMPTIONSlLO7 The four basic assumptions underlying GAAP are (1) the economic entity assumption, (2) the going concern assumption, (3) the periodicity assumption, and (4) the monetary unit assumption. Economic Entity Assumption. An essential assumption is that all economic events can be identified with a particular economic entity. Investors desire information about an economic entity that corresponds to their ownership interest. For example, if you were considering buying some ownership stock in FedEx, you would want information on the various operating units that constitute FedEx. You would need information not only about their United States operations but also about their European and other international operations. Also, you would not want the information about FedEx combined with that of United Parcel Service (UPS), another air freight company. These would be two separate economic entities. The financial information for the various companies (subsidiaries) in which FedEx owns a controlling interest (greater than 50% ownership of voting stock) should be combined with that of FedEx (the parent). The parent and its subsidiaries are separate legal entities but one accounting entity.

Another key aspect of this assumption is the distinction between the economic activities of owners and those of the company. For example, the economic activities of a sole proprietorship, Uncle Jim’s Restaurant, should be separated from the activities of its owner, Uncle Jim. Uncle Jim’s personal residence, for instance, is not an asset of the business. Going Concern Assumption. Another necessary assumption is that, in the absence of information to the contrary, it is anticipated that a business entity will continue to operate indefinitely. Accountants realize that the going concern assumptionin the absence of information to the contrary, it is anticipated that a business entity will continue to operate indefinitely. does not always hold since there certainly are many business failures. However, companies are begun with the hope of a long life, and many achieve that goal.

This assumption is critical to many broad and specific accounting principles. For example, the assumption provides justification for measuring many assets based on their historical costs. If it were known that an enterprise was going to cease operations in the near future, assets and liabilities would not be measured at their historical costs but at their current liquidation values. Similarly, depreciation of a building over an estimated life of 40 years presumes the business will operate that long. Periodicity Assumption. The periodicity assumptionallows the life of a company to be divided into artificial time periods to provide timely information. relates to the qualitative characteristic of timeliness. External users need periodic information to make decisions. This need for periodic information requires that the economic life of an enterprise (presumed to be indefinite) be divided into artificial time periods for financial reporting. Corporations whose securities are publicly traded are required to provide financial information to the SEC on a quarterly and annual basis.39 Financial statements often are prepared on a monthly basis for banks and others that might need more timely information.

For many companies, the annual time period (the fiscal year) used to report to external users is the calendar year. However, other companies have chosen a fiscal yearthe annual time period used to report to external users. that does not correspond to the calendar year. The accounting profession and the Securities and Exchange Commission advocate that companies adopt a fiscal year that corresponds to their natural business year. A natural business year is the 12-month period that ends when the business activities of a company reach their lowest point in the annual cycle. For example, many retailers, Wal-Mart for example, have adopted a fiscal year ending on January 31. Business activity in January generally is quite slow following the very busy Christmas period. We can see from the FedEx financial statements that the company’s fiscal year ends on May 31. The Campbell Soup Company’s fiscal year ends in July; Clorox’s in June; and Monsanto’s in August. FedEx Corporation Monetary Unit Assumption. Recall that to measure financial statement elements, a unit or scale of measurement must be chosen. Information would be difficult to use if, for example, assets were listed as “three machines, two trucks, and a building.” A common denominator is needed to measure all elements. The dollar in the United States is the most appropriate common denominator to express information about financial statement elements and changes in those elements.

One problem with this assumption is that the monetary unit is presumed to be stable over time. That is, the value of the dollar, in terms of its ability to purchase certain goods and services, is constant over time. This obviously does not strictly hold. The U.S. economy has experienced periods of rapidly changing prices. To the extent that prices are unstable, and those machines, trucks and building were purchased at different times, the monetary unit used to measure them is not the same. The effect of changing prices on financial information generally is discussed elsewhere in your accounting curriculum, often in an advanced accounting course. ACCOUNTING PRINCIPLESlLO8 There are four important broad accounting principles that provide significant guidance for accounting practice: (1) the historical cost principle, (2) the realization principle (also known as the revenue recognition principle), (3) the matching principle, and (4) the full-disclosure principle. These principles deal with the critical issues of recognition and measurement. The accrual accounting model is embodied in each of the principles. Historical Cost Principle. The FASB recognized in SFAC 5 that elements in financial statements currently are measured by different attributes. In general, however, GAAP measure assets and liabilities based on their original transaction value, that is, their historical costs.original transaction value. For an asset, this is the fair value of what is given in exchange (usually cash) for the asset at its initial acquisition. For liabilities, it is the current cash equivalent received in exchange for assuming the liability. For example, if a company borrowed $1 million cash and signed an interest-bearing note promising to repay the cash in the future, the liability would be valued at $1 million, the cash received in exchange.40

Why base measurement on historical costs? After all, the current value of a company’s manufacturing plant might seem more relevant than its original cost. First, historical cost provides important cash flow information as it represents the cash or cash equivalent paid for an asset or received in exchange for the assumption of a liability. Second, because historical cost valuation is the result of an exchange transaction between two independent parties, the agreed on exchange value is objective and highly verifiable. Alternatives such as measuring an asset at its current market value involve estimating a selling price. An example given earlier in the chapter concerned the valuation of a parcel of land. Appraisers could easily differ in their assessment of current market value.

There are occasions where a departure from measuring an asset based on its historical cost is warranted. Some assets, for instance, are measured at their net realizable value. For example, if customers purchased goods or services on account for $10,000, the asset, accounts receivable, would initially be valued at $10,000, the original transaction value. Subsequently, if $2,000 in bad debts were anticipated, net receivables should be valued at $8,000, the net realizable value. Departures from historical cost measurement such as this provide more appropriate information in terms of the overall objective of providing information to aid in the prediction of future cash flows.

Realization Principle. Determining accounting income by the accrual accounting model is a challenging task. When to recognize revenue is critical to this determination. Revenues are inflows of assets resulting from providing a product or service to a customer. At what point is this event recognized by an increase in assets? The realization principlerequires that the earnings process is judged to be complete or virtually complete, and there is reasonable certainty as to the collectibility of the asset to be received (usually cash) before revenue can be recognized. requires that two criteria be satisfied before revenue can be recognized:

These criteria help ensure that a revenue event is not recorded until an enterprise has performed all or most of its earnings activities for a financially capable buyer. The primary earnings activity that triggers the recognition of revenue is known as the critical event. The critical event for many businesses occurs at the point-of-salethe goods or services sold to the buyer are delivered (the title is transferred).. This usually takes place when the goods or services sold to the buyer are delivered (i.e., title is transferred).

The timing of revenue recognition is a key element of earnings measurement. An income statement should report the results of all operating activities for the time period specified in the financial statements. A one-year income statement should report the company’s accomplishments only for that one-year period. Revenue recognition criteria help ensure that a proper cut-off is made each reporting period and that exactly one year’s activity is reported in that income statement. Not adhering to revenue recognition criteria could result in overstating revenue and hence net income in one reporting period and, consequently, understating revenue and net income in a subsequent period. Notice that revenue recognition criteria allow for the implementation of the accrual accounting model. Revenue should be recognized in the period it is earned, not necessarily in the period in which cash is received. Some revenue-producing activities call for revenue recognition over time, rather than at one particular point in time. For example, revenue recognition could take place during the earnings process for long-term construction contracts. We discuss revenue recognition in considerable depth in Chapter 5. That chapter also describes in more detail the concept of an earnings process and how it relates to performance measurement.

Matching Principle. When are expenses recognized? The matching principleexpenses are recognized in the same period as the related revenues. states that expenses are recognized in the same period as the related revenues. There is a cause-and-effect relationship between revenue and expense recognition implicit in this definition. In a given period, revenue is recognized according to the realization principle. The matching principle then requires that all expenses incurred in generating that same revenue also be recognized. The net result is a measure—net income—that matches current period accomplishments and sacrifices. This accrual-based measure provides a good indicator of future cash-generating ability.

Although the concept is straightforward, its implementation can be difficult. The difficulty arises in trying to identify cause-and-effect relationships. Many expenses are not incurred directly because of a revenue event. Instead, the expense is incurred to generate the revenue, but the association is indirect. The matching principle is implemented by one of four different approaches, depending on the nature of the specific expense. Only the first approach involves an actual cause-and-effect relationship between revenue and expense. In the other three approaches, the relationship is indirect. An expense can be recognized:

The first approach is appropriate for cost of goods sold. There is a definite cause-and-effect relationship between Dell Inc.’s revenue from the sale of personal computers and the costs to produce those computers. Commissions paid to salespersons for obtaining revenues also is an example of an expense recognized based on this approach.

Unfortunately, for most expenses there is no obvious cause-and-effect relationship between a revenue and expense event. In other words, the revenue event does not directly cause expenses to be incurred. Many expenses, however, can be related to periods of time during which revenue is earned. For example, the monthly salary paid to an office worker is not directly related to any specific revenue event. The employee provides services during the month. The asset used to pay the employee, cash, provides benefits to the company only for that one month and indirectly relates to the revenue recognized in that same period.

Some costs are incurred to acquire assets that provide benefits to the company for more than one reporting period. Refer again to the Carter Company example in Illustration 1-1 . At the beginning of year 1, $60,000 in rent was paid covering a three-year period. This asset, prepaid rent, helps generate revenues for more than one reporting period. In that example, we chose to “systematically and rationally” allocate rent expense equally to each of the three one-year periods rather than to charge the expense to year 1.

The fourth approach to expense recognition is called for in situations when costs are incurred but it is impossible to determine in which period or periods, if any, revenues will occur. For example, consider the cost of advertising. Advertising expenditures are made with the presumption that incurring that expense will generate incremental revenues. Let’s say FedEx spends $1 million for a series of television commercials. It’s difficult to determine when, how much, or even whether additional revenues occur as a result of that particular series of ads. Because of this difficulty, advertising expenditures are recognized as expense in the period incurred, with no attempt made to match them with revenues.

The Full-Disclosure Principle. Remember, the purpose of accounting is to provide information that is useful to decision makers. So, naturally, if there is accounting information not included in the primary financial statements that would benefit users, that information should be provided too. The full-disclosure principlethe financial reports should include any information that could affect the decisions made by external users. means that the financial reports should include any information that could affect the decisions made by external users. Of course, the benefits of that information, as noted earlier, should exceed the costs of providing the information. Supplemental information is disclosed in a variety of ways, including:

We find examples of these disclosures in the FedEx financial statements in Appendix B located at the back of this text. A parenthetical or modifying comment is provided in the common stockholders’ investment section of the balance sheet with disclosure of the number of shares of stock authorized, issued, and outstanding. The statements include several notes as well as a supplemental statement disclosing information about the company’s quarterly operating results. Notice that the FedEx Corporation financial statements include the following statement: “The accompanying notes are an integral part of these consolidated financial statements.” We discuss and illustrate disclosure requirements as they relate to specific financial statement elements in later chapters as those elements are discussed. FedEx Corporation Graphic 1-8 provides a summary of the accounting assumptions and principles that guide the recognition and measurement of accounting information.

Brief-Exercises BE1-4, BE1-5, BE1-6 Exercises E1-8, E1-9, E1-10, E1-11, E1-12, E1-13 Judgment Case 1-11 Analysis Case 1-12 Real World Case 1-13 37 “Recognition and Measurement in Financial Statements,” Statement of Financial Accounting Concepts No. 5 (Stamford, Conn.: FASB, 1984), par. 63. 38 “Using Cash Flow Information and Present Value in Accounting Measurements,” Statement of Financial Accounting Concepts No. 7 (Norwalk, Conn.: FASB, 2000). 39 The report that must be filed for the first three quarters of each fiscal year is Form 10-Q and the annual report is Form 10-K. 40 This current cash equivalent for many liabilities also will equal the present value of future cash payments. This is illustrated in a subsequent chapter. |