|

| 1 | Barrick Company has established a flexible budget for manufacturing overhead based on direct labour-hours. Total budgeted costs at 200,000 direct labour-hours are as follows

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::Ad MCQs Ch13Q1::/sites/dl/free/0077121643/627780/CH13Q1.JPG','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif">Ad MCQs Ch13Q1 (34.0K)</a>Ad MCQs Ch13Q1 <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::Ad MCQs Ch13Q1::/sites/dl/free/0077121643/627780/CH13Q1.JPG','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif">Ad MCQs Ch13Q1 (34.0K)</a>Ad MCQs Ch13Q1

At an activity level of 170,000 direct labour-hours, the flexible budget for factory overhead would show the budgeted amount for utilities as

(Learning Objective 1 Ch 13) |

| A) | £85,000. |

| B) | £140,000. |

| C) | £160,000. |

| D) | £100,000. |

|

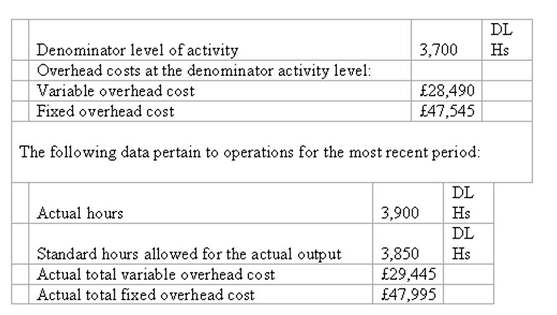

| 2 | A manufacturing company has a standard costing system based on direct labour-hours (DLHs) as the measure of activity. Data from the company's flexible budget for manufacturing overhead are given below:

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::Ad MCQs Ch13Q2::/sites/dl/free/0077121643/627780/Ch13Q2.JPG','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif">Ad MCQs Ch13Q2 (85.0K)</a>Ad MCQs Ch13Q2 <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::Ad MCQs Ch13Q2::/sites/dl/free/0077121643/627780/Ch13Q2.JPG','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif">Ad MCQs Ch13Q2 (85.0K)</a>Ad MCQs Ch13Q2

What was the variable overhead efficiency variance for the period, to the nearest pound?

(Learning Objective 2 Ch 13) |

| A) | £578 U |

| B) | £385 U |

| C) | £378 U |

| D) | £955 U |

|

| 3 | The overhead spending variance contains price but not quantity elements

(Learning Objective 3 Ch 13) |

| A) | True |

| B) | False |

|

| 4 | Waste or excessive usage of overhead items will show up as part of the variable overhead efficiency variance

(Learning Objective 4 Ch 13) |

| A) | True |

| B) | False |

|

| 5 | The economic impact of the inability to reach a target denominator level of activity would best be measured by:

(Learning Objective 5 Ch 13) |

| A) | the amount of the volume variance. |

| B) | the contribution margin lost by failing to meet the target denominator level of activity. |

| C) | the amount of the fixed overhead budget variance. |

| D) | the amount of the variable overhead efficiency variance. |

|

| 6 | The higher the denominator level of activity

(Learning Objective 6 Ch 13) |

| A) | the higher the cost per unit of product. |

| B) | the lower the cost per unit of product. |

| C) | the less likely is the occurrence of a volume variance. |

| D) | the more profitable operations likely will be. |

|

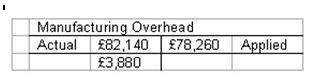

| 7 | At the end of the year, a company's Manufacturing Overhead account contained the following data:

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::Ad MCQs Ch13Q7::/sites/dl/free/0077121643/627780/CH13Q7.JPG','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif">Ad MCQs Ch13Q7 (15.0K)</a>Ad MCQs Ch13Q7 <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::Ad MCQs Ch13Q7::/sites/dl/free/0077121643/627780/CH13Q7.JPG','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif">Ad MCQs Ch13Q7 (15.0K)</a>Ad MCQs Ch13Q7

If the denominator activity for the year was 40,000 machine-hours, and if 36,400 machine-hours were allowed for the year's production, then the predetermined overhead rate per machine-hour was:

(Learning Objective 6 Ch 13) |

| A) | £2.15. |

| B) | £1.96. |

| C) | £2.26. |

| D) | £2.05. |

|

| 8 | Overhead is applied to work in process in a standard costing system by

(Learning Objective 6 Ch 13) |

| A) | multiplying actual hours times the predetermined rate. |

| B) | multiplying standard hours allowed for the output of the period times the predetermined rate. |

| C) | multiplying actual hours times the actual rate. |

| D) | multiplying standard hours allowed for the output of the period times the actual rate. |

|

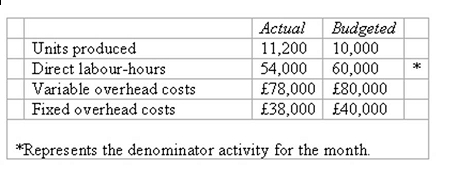

| 9 | French Business Unit produces and sells a single product, detailed below:

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::Ad MCQs Ch13Q9::/sites/dl/free/0077121643/627780/Ch13Q9.JPG','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif">Ad MCQs Ch13Q9 (48.0K)</a>Ad MCQs Ch13Q9 <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::Ad MCQs Ch13Q9::/sites/dl/free/0077121643/627780/Ch13Q9.JPG','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif">Ad MCQs Ch13Q9 (48.0K)</a>Ad MCQs Ch13Q9

The fixed overhead volume variance for March for the French Business Unit is

(Learning Objective 7 Ch 13) |

| A) | £1,555 favourable. |

| B) | £7,333 unfavourable. |

| C) | £2,667 unfavourable. |

| D) | £5,667 unfavourable. |

|

| 10 | The only difference between standard costing and activity based budgeting is that the cost formulas for variable overhead costs will be stated in terms of different kinds of activities instead of all being stated in terms of units or a common measure of activity such as direct labour-hours or machine-hours.

(Learning Objective 8 Ch 13) |

| A) | True |

| B) | False |